The Agentic Web: Inside the Protocol Race for Machine-to-Machine Payments

Stripe and Coinbase are building competing rails for how AI agents will pay for things. The winner will sit beneath the next trillion-dollar payments market.

The internet has a payment problem it didn’t know it had. Every rail underneath modern commerce, from Visa to ACH to SWIFT, was built on the same assumption: a human is ultimately responsible for authorizing what happens. That assumption is about to break. AI agents now write code, book meetings, scrape data, and provision infrastructure. The next generation will spend money. None of the infrastructure they need to do that exists yet. Two companies are building it right now.

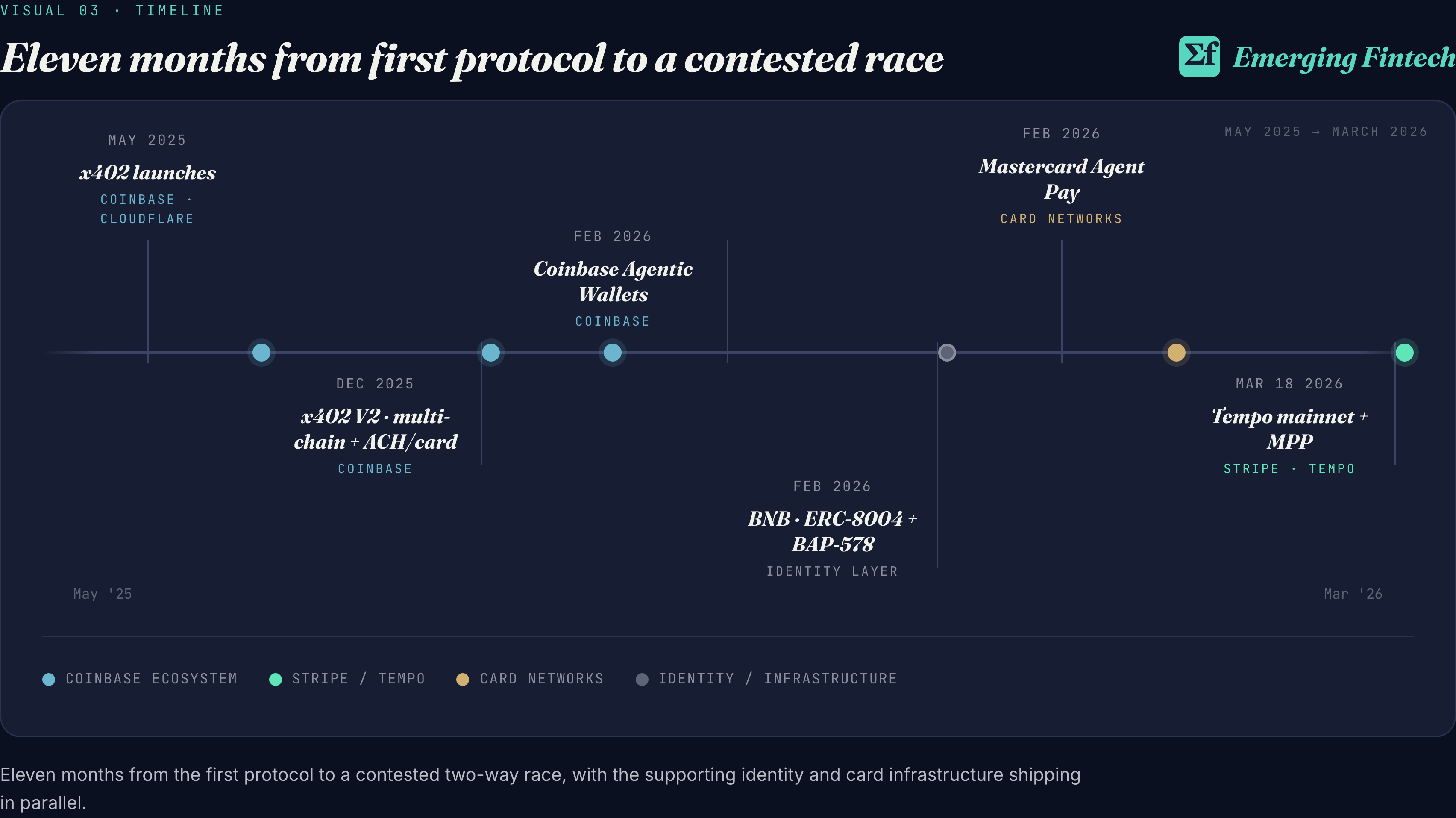

Coinbase shipped x402 in May 2025, a developer-first protocol that embeds payments directly into HTTP. It processed over 100 million transactions in its first six months. Stripe and Tempo countered on March 18, 2026, with the Machine Payments Protocol, an enterprise-first standard launched alongside a $5 billion blockchain and a directory of 100+ integrated services. Each is backed by one of the most important companies in technology. Each approaches the problem from a different angle. The protocol that wins will sit beneath the economic layer of the agentic web. The agentic web is internet activity in which AI agents request resources, transact with services, and pay other agents on behalf of the entities that deployed them.

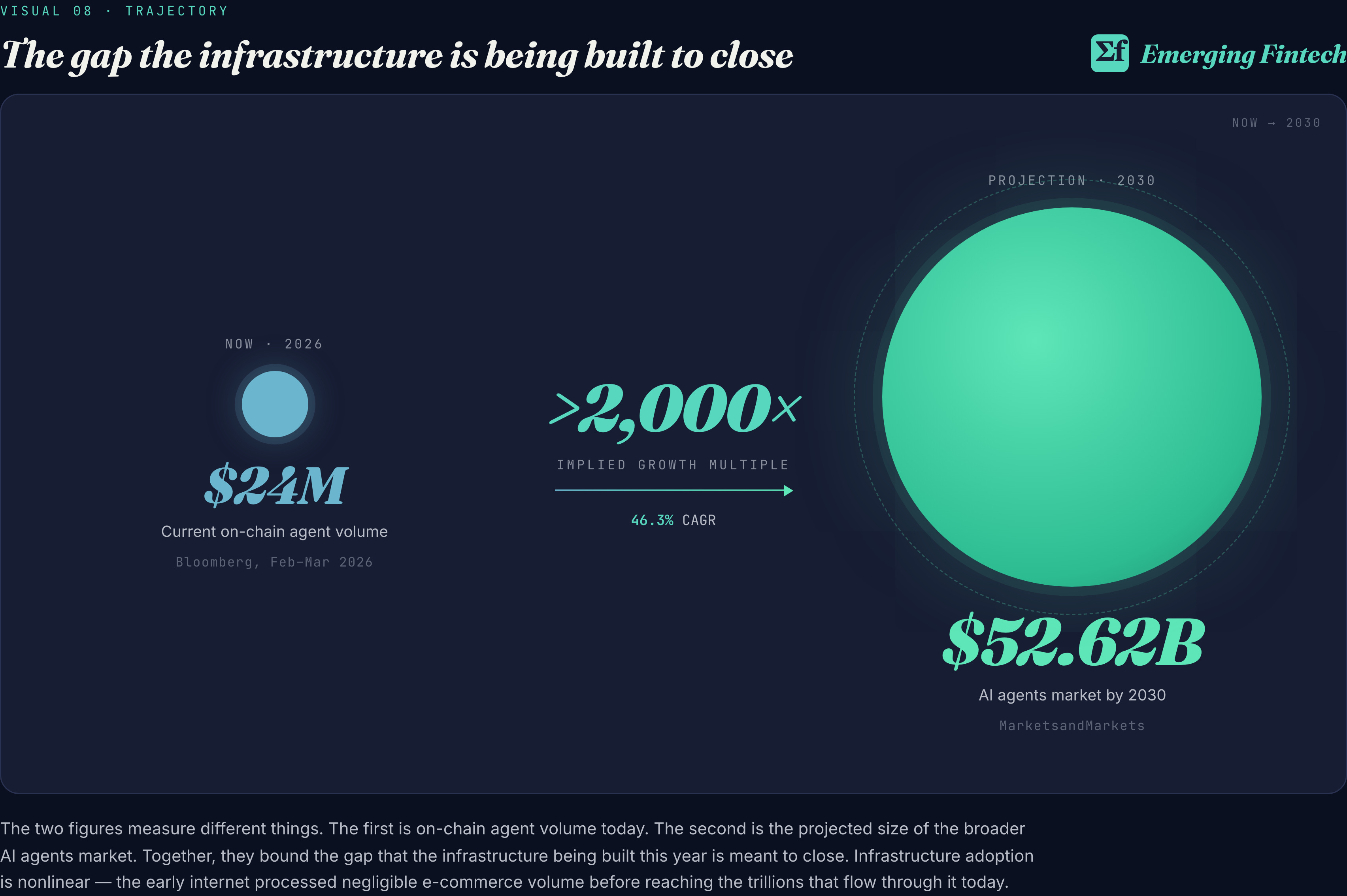

The market being built for is worth approximately $24 million today, according to Bloomberg's March 2026 reporting on transaction volumes between February and March of this year. An a16z partner has noted that after filtering out wallets trading with themselves, the real on-chain agent volume is closer to $1.6 million. Either figure is a rounding error against global payments volumes measured in hundreds of trillions. The infrastructure being standardized right now assumes that gap will close fast.

The signal worth pausing on is who Stripe chose as design partners on MPP. Visa and Shopify are unsurprising. OpenAI and Anthropic are the actual story. A payments company that processed $1.9 trillion in 2025 brought two AI labs into the design room for its next-generation standard. The customer being designed for is no longer human.

This piece walks through why these protocols exist, how they differ, and where the most durable investment opportunities sit.

Welcome to Emerging Fintech 👋🏻, your weekly deep dive into venture capital and fintech across emerging markets. If someone forwarded this to you, subscribe to get insights like this delivered weekly.

This edition is sponsored by Angel Squad - Join 2,000+ members from Apple, Nike, Stripe & Meta learning Hustle Fund’s proven frameworks. Access curated deals from our 1,000+ monthly pipeline (we share the top 0.5%), weekly live pitch sessions, and global networking in 20+ cities. Squad members have invested $30M+ in 70+ companies alongside Hustle Fund. Start your 30-day free trial → https://go.angelsquad.co/gBk0

Why the Internet Was Never Built for Agents

Every payment rail in use today assumes a human is ultimately responsible for authorizing what happens. Credit cards require a cardholder. Bank transfers require an account holder. OAuth tokens require someone to log in. API keys are issued to developers, not to software. Every rail was designed around a human authorization chain.

AI agents break all of those assumptions.

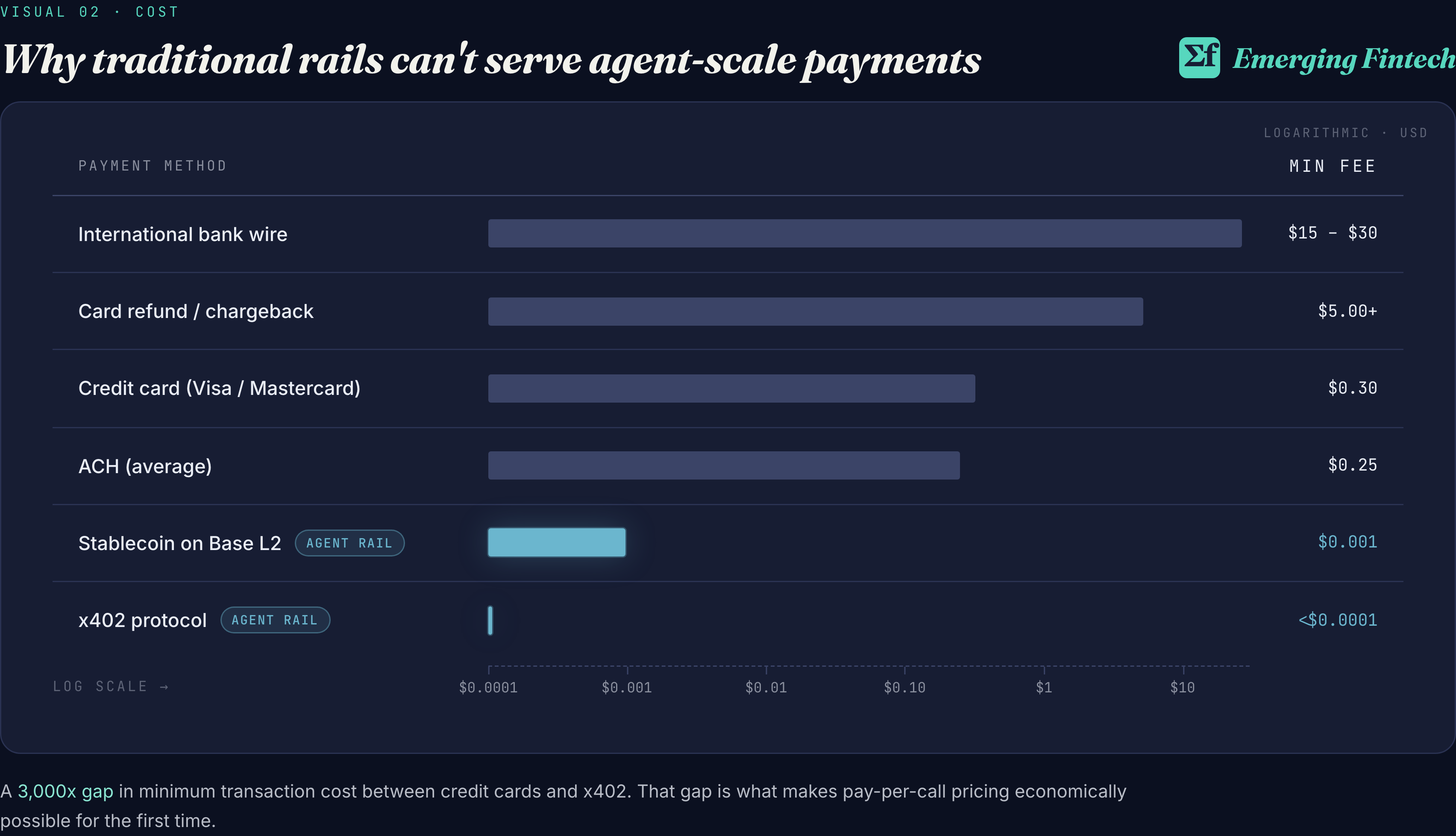

There are three reasons the existing infrastructure cannot accommodate them. The first is pricing. Credit card fees of roughly $0.30 per transaction make micropayments mathematically impossible. An API request cannot be priced at $0.001 when the rail charges three hundred times that amount per transaction. Subscription models are a workaround that averages demand across time, but they break the pay-per-use logic that agent workflows require. An agent that consumes three API calls should not pay for thirty days of access.

The second is identity. Traditional banking rails require a verifiable human account holder under KYC. Coinbase CEO Brian Armstrong noted publicly in early 2026 that AI agents cannot meet Know Your Customer requirements and therefore cannot use traditional banking infrastructure. This is a structural mismatch, not a regulatory edge case.

The third is settlement, and it is the largest of the three. Cross-border payments settle in one to three days through correspondent banking, at unpredictable cost. For an agent executing thousands of micropayments per hour across jurisdictions, that is a hard stop. Stablecoins offer an answer. Global stablecoin volumes doubled to $400 billion in 2025, with 60% of that volume now attributable to B2B activity. The shift from speculative to commercial use is the foundation on which the entire agentic payments stack is being built.

The $190 trillion annual cross-border payments market is the clearest illustration of the gap, and the prize.

The Two Protocols That Matter

The rails to capture that prize are being built right now. Coinbase shipped first. Stripe shipped second. Google released a coordination protocol called AP2 in September 2025 that handles agent-to-agent messaging and routes payments through x402 underneath, which makes it more an extension than a third competitor. The serious race is between two protocols.

x402: Payments Embedded in HTTP

Coinbase launched x402 in May 2025 alongside the x402 Foundation, co-established with Cloudflare. The protocol revives the long-dormant HTTP 402 “Payment Required” status code to embed payments directly into web interactions.

A client sends a standard HTTP request. The server responds with a 402 status code and payment instructions: amount, accepted currency, destination wallet. The client attaches a signed payment payload, retries the request, and the facilitator settles the transaction on-chain. Access is granted. No new communication layer is introduced. It extends native HTTP behavior.

Transaction fees sit below $0.0001. That makes micropayments practical for the first time. An agent can pay $0.001 for an API request or fractions of a cent per data query. In its first six months, x402 processed over 100 million payments. V2, released in December 2025, added multi-chain support by default and compatibility with legacy rails including ACH and card networks. Key integrations include Circle, Alchemy, Visa TAP, and Stripe’s own agentic commerce work. Cloudflare’s “pay per crawl” beta lets developers fetch web data and settle payments in the same request cycle. MCP servers can now expose paid tools that Claude, Gemini, and other LLMs can access natively.

MPP: The Enterprise Standard

If x402 is the open-internet answer, MPP is the enterprise one. Stripe and Tempo launched the Machine Payments Protocol on March 18, 2026. Tempo is a Layer 1 blockchain incubated by Stripe and Paradigm, built specifically for high-volume payment workloads. It has no native gas token. Fees settle in major stablecoins. It is ISO 20022 compliant, which is the international financial messaging standard used by global banks. Tempo raised $500 million at a $5 billion valuation, with Thrive Capital leading.

The core innovation of MPP is the “session” primitive. Think of it as OAuth for payments. An agent authorizes once and pre-funds its account. Every subsequent API call or resource consumption triggers real-time automatic settlement without a separate on-chain transaction. Thousands of small transactions aggregate into a single settlement event. That solves the reconciliation problem that makes micropayments operationally complex for enterprises.

MPP runs on Tempo but is rail-agnostic. Visa extended it to card payments. Stripe added support for wallets and other payment methods through its existing platform. Lightspark integrated Bitcoin payments over Lightning. The launch directory lists over 100 compatible services. Klarna announced a stablecoin launch on Tempo.

Stripe processed $1.9 trillion in total payment volume in 2025, a 34% year-on-year increase. MPP is Stripe’s deliberate infrastructure bet on where commerce is heading.

Like this article? Subscribe for more fintech analysis.

Developer-First vs Enterprise-First: A Familiar Pattern

Both bets are serious. They are also different bets, aimed at different segments of the market. The x402 vs MPP contest is not unprecedented. The history of payment infrastructure is full of developer-first protocols competing against enterprise-first standards, and the typical outcome is not a single winner. It is segmentation.

Stripe is the clearest case. When it launched in 2010, the existing rails were ACH and the card networks, both designed for enterprise integration. Stripe won developers by collapsing weeks of integration work into seven lines of code. ACH and Visa never went away. They handle different jobs today than Stripe does, and they coexist. The market segmented along the line between developer-first and enterprise-first.

The same pattern played out in cloud infrastructure. AWS won developers while incumbent enterprise IT retained legacy workloads. Twilio did the same to legacy SMS aggregators. Wise did the same to SWIFT in international payments. In each case, the developer-first option captured the long tail of new use cases while the enterprise-first incumbent retained the high-volume, regulated core.

x402 fits the developer-first pattern cleanly. It is permissionless and lightweight, optimized for the long tail of micropayment use cases that traditional rails cannot price. MPP fits the enterprise-first pattern equally cleanly. It is ISO 20022 compliant, distributed through Stripe’s existing platform, and extended by Visa to card networks. The design target is organizations that need integration with existing reconciliation infrastructure.

The reasonable base case is that both protocols persist. x402 captures the pay-per-call long tail and the agent-native services that have no enterprise analog. MPP captures the high-volume, audit-required workloads that enterprise procurement and treasury functions need. The interesting investment question is not which one wins. It is which categories each owns, and where the abstraction layer that bridges them lives.

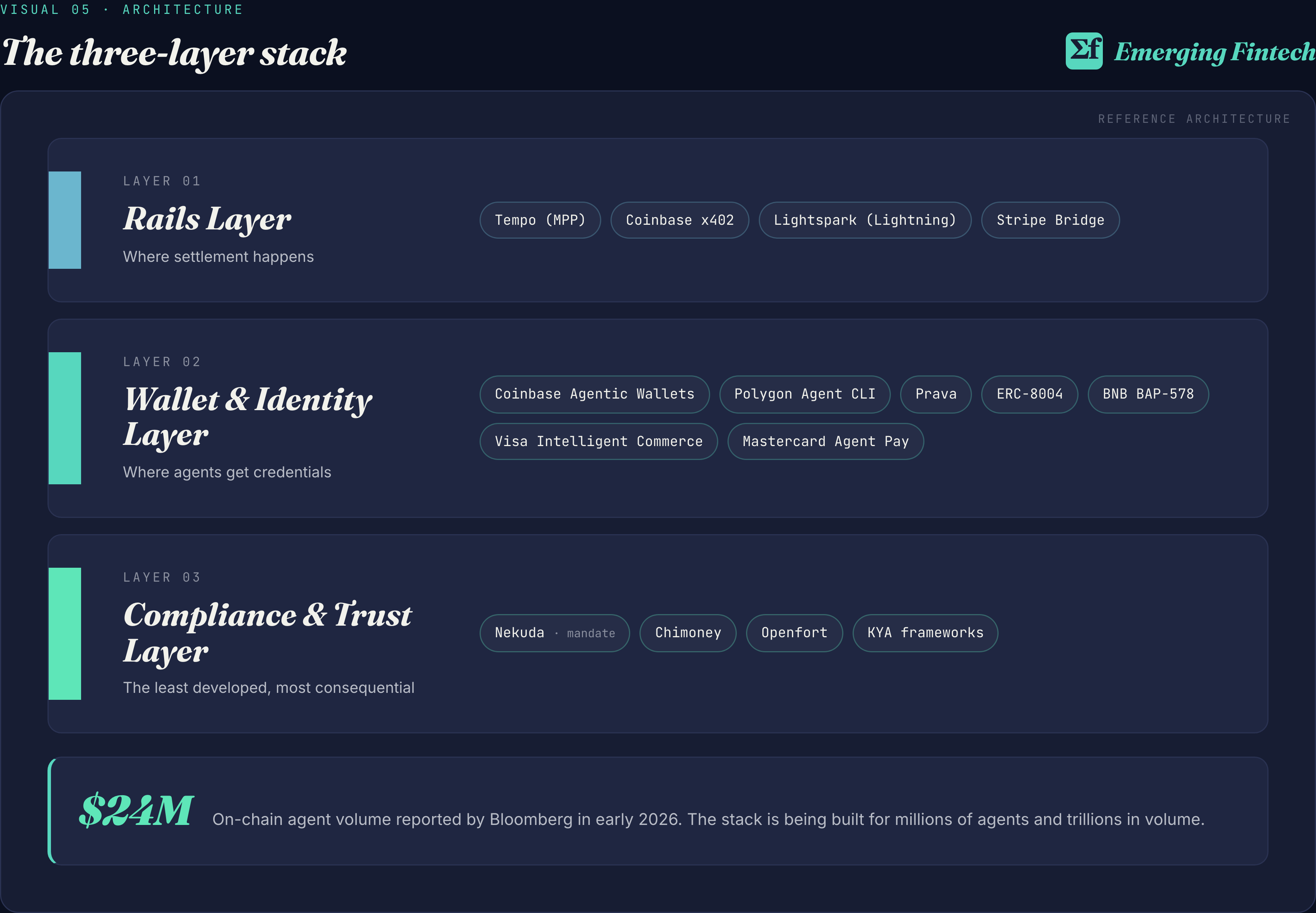

The Stack: Rails, Wallets, Compliance

Underneath the protocol layer, the agentic payments stack divides into rails, wallets, and compliance. Each is contested. None are solved.

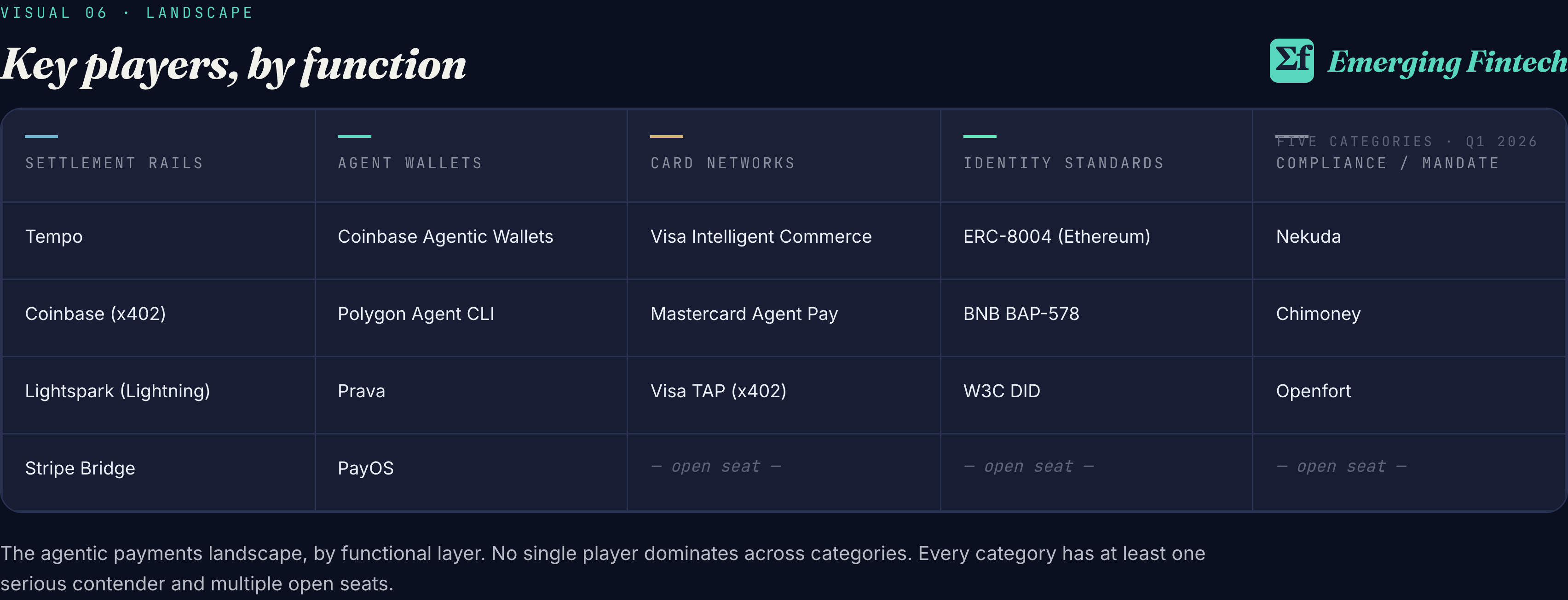

The rails layer is where settlement happens. Tempo, x402 on Base and Solana, Lightspark on Bitcoin Lightning, and Stripe Bridge for stablecoin-to-fiat are the primary players. Each represents a different architectural bet: a dedicated L1 optimized for payments, protocol extension on existing L1s, Bitcoin-native, or fiat-bridged stablecoin infrastructure.

The wallet and identity layer is where agents get their credentials, and it is where the most production work is happening this year. Coinbase launched Agentic Wallets in February 2026, the first wallet infrastructure purpose-built for AI agents. These wallets provide programmable spending policies, non-custodial identity, and permissioned execution. Spending limits are enforced before any transaction executes. KYT screening blocks high-risk interactions automatically. At the standards level, ERC-8004 is the emerging Ethereum standard for on-chain agent identity, co-authored by MetaMask, Google, the Ethereum Foundation, and Coinbase. The standard went live on Ethereum mainnet on January 29, 2026. BNB Chain followed in February with its own deployment alongside BAP-578, which introduced Non-Fungible Agents: software entities that exist as on-chain assets, own wallets, and can hold and spend funds. On the card side, Visa’s Intelligent Commerce initiative is working with over 100 partners globally. Mastercard’s Agent Pay uses Agentic Tokens, dynamic digital credentials that bring tokenization from mobile payments into agentic commerce.

The compliance and trust layer is the least developed part of the stack, and the most consequential. Payment regulations like PSD2 and Strong Customer Authentication require clear human authorization for payment orders. No current regulatory mechanism treats an AI agent as equivalent to a human payer. This gap is not a technical problem. It is a regulatory one, and closing it will define the ceiling for how much volume agentic commerce can reach in the near term.

The concept of KYA, for Know Your Agent, is emerging as the compliance framework for this space. Every agent will eventually need a verifiable digital identity anchored to a legal entity, a smart wallet with programmable constraints, and a reputation record built on past behavior. The useful analogy is a corporate employee with a prepaid card. Rules exist. Limits are set. Activity is monitored. Accountability flows back to the entity that deployed the agent.

Four Investment Themes

That is the stack being built. The question for builders and investors is which layers get monetized first, and by whom. Four durable themes emerge from the protocol landscape, each at a different stage of development.

Protocol infrastructure follows winner-take-most dynamics. Payment protocol adoption historically follows winner-take-most dynamics, but not winner-take-all. Visa and Mastercard coexist. TCP/IP runs on different physical infrastructure. The more relevant question is whether agentic payments fragment by use case or whether one standard achieves enough early adoption to become the default across uses. x402’s 100 million transactions in six months reflect developer-first adoption, the same pattern that built Stripe and Twilio into category leaders. MPP’s launch with Stripe, Visa, and a 100+ service directory reflects enterprise-first adoption, the same pattern that built SWIFT and ACH into durable infrastructure. Both approaches have historical precedent. The investment thesis for protocol-adjacent infrastructure does not depend on picking the winning protocol. Facilitators, settlement verification, multi-protocol abstraction layers, and developer tooling that normalizes across MPP and x402 will be durable plays as long as multiple standards remain in play.

The most interesting early-stage opportunity sits at the identity layer. The problem is well-defined and unsolved. Agents need verifiable credentials. Credentials need to anchor to accountable legal entities. Spending behavior needs to be auditable. The whole system needs to work without requiring human approval at each transaction. None of the solutions that exist today are production-ready at scale. ERC-8004 is an emerging standard, not a deployed product. Coinbase Agentic Wallets provide infrastructure but not the compliance layer that regulated industries require. The Banking-as-a-Service parallel is instructive. When community banks started partnering with fintech companies at scale in the late 2010s, the compliance gap between what banks were required to enforce and what technology companies could manage produced years of consent orders, regulatory friction, and market restructuring. Agentic payments is likely to follow the same arc, with early enthusiasm giving way to compliance reckoning before the category restructures. Companies that build KYA tooling before the reckoning arrives will be well-positioned.

B2A is becoming a real revenue category. Agents have fundamentally different consumption patterns than humans. They pay per task, per API call, per data query. SaaS sells subscriptions to humans. B2A sells capabilities to agents. Browserbase, which lets agents spin up headless browsers and pay per session via MPP, is one early example. PostalForm, which lets agents pay to print and send physical mail, is another. These are agent-native services with no direct human analog. The investment question is which existing software categories get repriced for agent consumption first. Data APIs are the most obvious target. Pay-per-query has always made more sense than subscription access for high-volume machine consumers, and the economics only improve at agent scale. Developer infrastructure is next. Compute is the obvious one. Storage and inference will follow.

Developer tooling for agent payments is wide open. Despite rapid progress on protocol and wallet infrastructure, the developer experience for building agent-native payments remains difficult. Integrating MPP requires familiarity with both stablecoin infrastructure and Stripe’s existing APIs. x402 is simpler at the HTTP layer but requires understanding on-chain settlement and facilitator mechanics. The companies that abstract this complexity effectively, presenting a clean interface for developers who want to add payment capability to an agent without becoming payments engineers, will capture significant value. This is the same arc that built Stripe itself from 2010 onward.

Risks

The opportunity is real. The path to capturing it is not clear. Four structural risks will shape how quickly this market develops.

Protocol fragmentation is the most immediate. Two competing open standards launched within ten months of each other, with Google’s coordination layer adding a third surface area. If MPP and x402 remain incompatible silos with high switching costs between them, developers will consolidate on one and the other will atrophy, or both will persist in separate verticals with the overhead that multi-protocol environments always impose. The middleware providers that abstracted away the complexity of multi-bank relationships in BaaS ultimately could not sustain the model. Multi-protocol abstraction in agentic payments could face a similar challenge.

What happens when an AI agent makes a payment that violates strong customer authentication? No one knows yet. PSD2, AML, and strong customer authentication frameworks all assume a human authorization chain. Until regulators provide clear guidance on how agentic payment flows should be governed, enterprises in regulated industries will face legal uncertainty that slows adoption. The CFPB’s 2025 pullback from BNPL oversight, after years of preparing to regulate the category, showed how regulatory posture can shift quickly in fintech. Agentic payments could face the same volatility.

LLM provider concentration creates a systemic risk that is often underappreciated. Agents operate inside inference environments controlled by a small number of providers. If those providers become chokepoints in the agent economy, they effectively control which agents can transact with which services. The identity frameworks being built today need to be model-agnostic and portable to avoid this concentration risk materializing.

A compromised agent with a funded wallet and broad spending authorization is a category of event with no precedent. A compromised human account is a localized incident. The spending-limit and KYT infrastructure being built into Coinbase Agentic Wallets and Nekuda’s mandate model are early responses, but they will not be sufficient once agent volumes reach the scale that makes these systems a meaningful attack target.

The Takeaway

None of these risks change the direction of travel. They change the timeline.

The infrastructure being built this year is the foundation for a payments ecosystem where software is the primary economic actor. MPP and x402 are not competing fintech products. They are competing proposals for how the internet should work when machines are the ones spending money.

The market is small today. Roughly $24 million in on-chain agent volume against a global payments backdrop measured in hundreds of trillions. Infrastructure adoption is nonlinear. The early internet processed negligible e-commerce volume before reaching the trillions that flow through it today.

The protocols being standardized this year will determine which companies sit underneath the agent economy when it scales. The companies that own those rails will own the economic layer of the agentic web.

Sources

Stripe and the Machine Payments Protocol (MPP)

- Stripe, ”Introducing the Machine Payments Protocol”, March 18, 2026

- Fortune, ”Stripe-backed crypto startup Tempo releases AI payments protocol, launches blockchain”, March 18, 2026

- The Defiant, ”Tempo Goes Live on Mainnet, Unveils Machine Payments Protocol with Stripe”, March 18, 2026

- CoinDesk, ”Stripe-led payments blockchain Tempo goes live with AI agent protocol”, March 18, 2026

- Ledger Insights, ”Stripe, Paradigm launch Tempo blockchain alongside machine payments standard”, March 20, 2026

Coinbase and the x402 Protocol

- Coinbase Developer Platform, ”Introducing x402: a new standard for internet-native payments”, May 2025

- x402 Foundation, ”Introducing x402 V2: Evolving the Standard for Internet-native Payments”, December 2025

- The Block, ”Coinbase-incubated x402 payments protocol built for AIs rolls out V2”, December 11, 2025

- Cloudflare, ”Launching the x402 Foundation with Coinbase, and support for x402 transactions”, December 3, 2025

Coinbase Agentic Wallets

- Coinbase Developer Platform, ”Introducing Agentic Wallets: Give Your Agents the Power of Autonomy”, February 11, 2026

- The Block, ”Coinbase rolls out AI tool to ‘give any agent a wallet”, February 13, 2026

- PYMNTS, ”Coinbase Debuts Crypto Wallet Infrastructure for AI Agents”, February 11, 2026

ERC-8004 Identity Standard

- Ethereum Improvement Proposals, ”ERC-8004: Trustless Agents”, August 2025

- Allium, ”Onchain AI identity: what ERC-8004 unlocks for agent infrastructure”, February 2026

- QuickNode, ”ERC-8004: A Developer’s Guide to Trustless AI Agent Identity”, March 4, 2026

Market Sizing and Agent Volumes

- Bloomberg, ”Stablecoin Firms Bet Big on AI Agent Payments That Barely Exist”, March 7, 2026

- Bloomberg, ”The Race to Bank AI Agents in New Era of Commerce Is Heating Up”, March 17, 2026

- Bloomberg, ”Coinbase, Cloudflare, Stripe Push to Shape Future of AI Money”, April 2, 2026

we noticed this x402 vs MPP framing across multiple crypto and vc newsletters this month, the identity layer is where the real money will get made